Driver update – On China risky policy shifts

The drop in the copper market is obviously the direct consequence of the FX policy shift in China. The shift is creating unintended consequences due to financial linkages, and here it is one the most well-known part of some of the Chinese carry trades (copper collateral) that is unwinding quickly. It has no importance in itself, but as an early indicator of credit bubble burst and eventual contagion it is very important. So it definitely has to be seen in relation to the moves we have seen two weeks ago on the CNY-CNH and on the Chinese Ted Spread.

Of course one can argue – as all investors currently do – that 1/ the Chinese authorities have a good policy track record (I would moderate that because in a credit bubble, your policy is always good until the bubble bursts… anyone remembers the god like status of Alan Greenspan before 2008?), 2/ that the Chinese authorities have the financial resources to deal with the recapitalization of any financial institutions / trust / companies threatened so the shadow banking system is not such an issue, 3/ the real risk is real estate.

I agree, those points make sense, except that in all bubbles, there are some financial dimensions and interlinkages that are always misunderstood. And it is often when policy makers try to deal with these bubbles that they end up making mistakes as they disturb the unsteady balance that has been the source of massive position accumulation. Moreover the unsteady financial equilibrium that lasted for at least 5 years is now facing not one but three major changes. First the Fed is reducing its liquidity ceteris paribus (see Yellen below); Second China is slowing; and Third it is in the process of liberalizing its capital account and dealing with its shadow banking system. All three policy shifts involve major risks. [On the topic of LT implications of China’s capital accounts liberalization – read this excellent paper from the BoE].

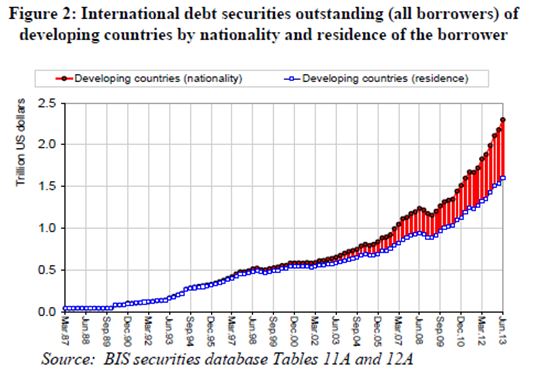

The big unknown here of course is how much of the Chinese credit bubble and corporate carry trades have been affecting global markets? How many (EM?) financial institutions are involved? The general opinion is not much, and things are under control, at least on the financial side. But what do we know exactly? The BIS and the IMF recently wrote two excellent pieces explaining how EM corporates were involved in massive balance sheet carry trades through their subsidiaries, and creating FX exposure that were not apparent in external debt balance of payment reporting (see the 2 graphs below). What I find really instructive in these papers is that many financial mechanisms / behaviors are not reported properly in international statistics, so we can’t really assess the risks … In other words we know that we don’t know everything, and that every bubble creates some new financial mechanisms.

The situation in China is probably even more opaque given that companies have been doing their best to avoid capital controls for years.

Yellen explained clearly four years ago (I doubt she would repeat that today) how US monetary conditions were affecting China: “China restricts capital inflows and outflows. These restrictions provide considerable—but not complete—insulation from foreign monetary policies and give the People’s Bank of China scope to conduct independent monetary policy. However, investors find ways to evade China’s capital controls and are pouring in money to take advantage of higher interest rates, a booming stock market, and an apparent gamble with only upside risk on future renminbi appreciation”.

More recently the FT explained in details the Chinese Corp carry trade – borrowing in USD abroad (0.25%), converting to CNY and investing in Trust products (5 to 10%)… [Doesn’t it sound like Easy money and win win trades…?] So for sure Copper is another warning sign. It might stop there. But there might also be contagion. The FT reported recently that Hong Kong and Singapore banks were heavily involved. So investors should be very attentive to any other sign of side effects in the coming weeks. I guess the first two things to watch is whether Copper breaks the $300 level, and how Hong Kong and Singapore banks and equity markets will react. That would be important signs of contagion… (and the SPX is not priced for that).

When I think about China’s policy situation, I can’t help but think of the HuaShan path (a sacred Taoist mountain that I climbed a few years ago). It is going up, it is gorgeous, everything is great… but the path is very narrow and slippery, so you’d better not fall either side because it’s a free fall guaranteed… (see below).